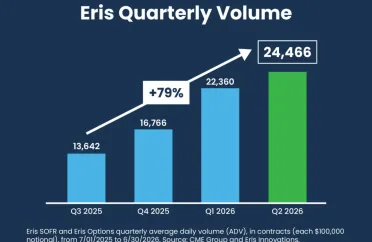

June capped a record quarter for Eris SOFR and Eris Options, with quarterly volume reaching 24,466 contracts, up 9% from the previous record (Q1 2026), and up 29% from Q2 last yearMonthly ADV of 49,888 contracts also set a new record, besting the previous record (March, 44,863) by 11%, with total volume surpassing one million contracts ($100 billion notional) for the first time in history

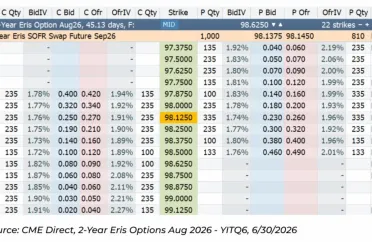

CME Group Eris Options have active order books with market makers now streaming two-sided prices. June trading totaled 1,222 contracts, with initial activity focused in the 2-year July expiry, as well as 2-year October and 10-year September.

Eris SOFR quarterly volume sets new records in May. Eris SOFR volume continued its recent growth in May, with rolling quarterly ADV setting an all-time record of 23,849 on May 22

By Edward Bolingbroke(Article available only to Bloomberg subscribers)Bloomberg features Eris Innovations’ latest funding round alongside the growing institutional adoption of Eris SOFR Swap futures.Read Bloomberg article

window.dataLayer = window.dataLayer || [];

function gtag(){dataLayer.push(arguments);}

gtag('js', new Date());

gtag('config', 'G-G640VE0Y19');

Leading trading firms invest in Eris Innovations amid growing demand for capital-efficient listed derivativesCHICAGO, IL — May 19, 2026 — Eris Innovations, an intellectual property licensing company and the creator of Eris SOFR Swap futures (Eris SOFR), today announced a new investment round backed by leading trading firms, following a marked rise in Eris SOFR activity at CME Group.Eris Innovations completed the investment round to support the launch of Eris Options in June, as well as the continued growth of the Eris SOFR complex, providing capital and strategic alignment with core liquidity providers. Participants include proprietary trading firms and their affiliates such as DRW, DV Trading, BlackEdge Capital, Arb Trading Group, Chicago Trading Company, and TransMarket Group, with DV Trading leading the round. CME Ventures also participated in the transaction.Recent activity in Eris SOFR reflects accelerating institutional adoption:Open interest tripled over a 16-month period from January 2025 to April 2026, increasing from 237,000 to a recent high of 713,000 contractsDuring the same period, the number of market participants more than doubled, according to CFTC public reports, reflecting expanding engagement from mortgage hedgers, regional banks, and asset managersAverage daily trading volume exceeded 22,000 contracts in the first quarter of 2026, including a monthly record of 44,863 contracts in MarchGrowing numbers of participants are accessing liquidity from both swap dealers and futures market makers to hedge interest rate risk using Eris SOFR, achieving initial margin savings of more than 60% compared with traditional OTC swapsEris Options are designed to deliver swaption-like risk exposure in a standardized, exchange-traded format. The product extends the capital efficiency and operational advantages of Eris SOFR into the options market, offering market participants a new way to manage longer-dated SOFR rate risk.“The rapid adoption of Eris SOFR demonstrates strong demand for liquid, capital-efficient, listed alternatives to OTC interest rate products,” said Michael Riddle, Chief Executive Officer of Eris Innovations. “This round aligns us with experienced liquidity providers critical to establishing deep, transparent markets for Eris Options.”“Eris SOFR Swap futures unlocked a more efficient way to access swap spread risk, combining the precision of OTC markets with the efficiency of listed derivatives,” said Don Wilson, CEO of DRW and co-inventor of the technology behind Eris Innovations. “The introduction of options extends that framework by offering more efficient ways of managing swap spread risk in the volatility space.”“Buy-side hedgers and fund managers are savvier than ever these days, constantly evaluating how to deploy their capital most efficiently to reach their investment objectives, lest they fall behind their competitors,” said Jared Vegosen, Co-Founder of DV Trading. “Having provided liquid markets in Eris SOFR since inception, we are focused on bringing the same depth, consistency, and pricing discipline to Eris Options at launch.”“SOFR underlies the vast majority of U.S. dollar floating-rate financing, and there is clear demand for more efficient tools to manage volatility in longer-dated exposures,” said Josh Mateffy, Founder and Managing Partner of BlackEdge Capital. “As a leading market maker in CME Group’s interest rate options for more than a decade, BlackEdge is well positioned to help build deep, consistent markets for Eris Options.”Eris Options will complement CME Group’s existing U.S. Treasury and SOFR complexes. Eris Options feature futures-style margining, similar to forward-premium OTC swaptions, and remove operational burdens associated with swap data repository (SDR) reporting, uncleared margin rules (UMR), and manual trade confirmations. About Eris InnovationsEris Innovations is an intellectual property licensing company that partners with global financial exchanges to develop futures products based on its patented product design, the Eris Methodology. Trademarks of Eris Innovations and/or its affiliates include Eris, Eris Innovations, Eris SOFR, Eris Options, and Eris Methodology. For more information on Eris Options, visit erisfutures.com/options. Media contact:Craig Haymakercraig.haymaker@erisfutures.com+1-952-952-6304Read more on Business Wire

window.dataLayer = window.dataLayer || [];

function gtag(){dataLayer.push(arguments);}

gtag('js', new Date());

gtag('config', 'G-G640VE0Y19');

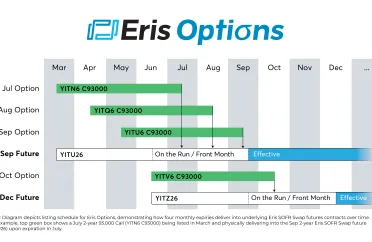

CME Group unveils Eris Options contract specificationsNote: Diagram depicts listing schedule for Eris Options, demonstrating how four monthly expiries deliver into underlying Eris SOFR Swap futures contracts over time. For example, top green box shows a July 2-year 93.000 Call (YITN6 C93000) being listed in March and physically delivering into the Sep 2-year Eris SOFR Swap future (YITU26) upon expiration in July.Following the recent press release announcing the June launch of Eris Options, CME Group released the Eris Options 2-page tearsheet, which includes detailed contract specificationsEris Options offer swaption-style risk in listed CME Group options, with four consecutive European-style monthly expiries (e.g., Jul, Aug, Sep, Oct) that physically deliver into 2-year, 5-year, or 10-year Eris SOFR Swap futuresEris Options feature futures-style margining, similar to forward-premium OTC swaptionsThey remove operational burdens associated with swap data repository (SDR) reporting, uncleared margin rules (UMR), and manual trade confirmationsFor more information, visit erisfutures.com/optionsNew Eris SOFR Market Maker: Bank of MontrealThe BMO swap desk is the most recent dealer to start responding to inquiries for Eris SOFR block trades“We are pleased to respond to the growing end user demand for Eris SOFR Swap futures by providing block trade liquidity across the swap curve,” said Akash Agrawal, Head of US Rates, Bank of MontrealFutures brokers can contact Akash Agrawal, Wesley Hyde, or Mike Novack on Bloomberg IB chat, and BMO clients can contact their BMO sales coverageClick here for a full list of Eris SOFR Block Market MakersOpen interest cracks 710,000 contractsEris SOFR Open interest (OI) reached 713K contracts ($71B notional) on Apr 28, finishing the month at 697K contractsOI in Eris SOFR Swap futures tripled over a 16-month period from January 2025 to April 2026, increasing from 242,000 to the recent high of 713,000 contractsOI leapt 158% year-over-year (YoY), up 427K contracts ($42.7B notional) from April 2025Mega blocks boosted OI including three Apr 17 trades, each greater than 7,500 contracts ($750mm notional)April activity follows record Q1 daily volume of 22,000 contracts, and record March daily volume of 44,000 contractsNew CME Group article: Unlocking Capital with Eris SOFREric Leininger of CME Research and New Product Development released a new article on reducing capital with Eris SOFR Swap futuresIt begins, “In the current landscape of shifting interest rate cycles and tightening liquidity, institutional hedgers are facing a silent drain on their balance sheets: initial margin (IM).”It notes, “the era of set-and-forget OTC hedging is over. As capital costs remain elevated, the ability to reduce margin …by 60% is a competitive necessity.”For similar risk transfer, insurers, banks, and asset managers achieve more capital flexibility with less balance sheet dragExplore initial margin comparisons between Eris SOFR and cleared OTC swaps at erisfutures.com/marginsavings

window.dataLayer = window.dataLayer || [];

function gtag(){dataLayer.push(arguments);}

gtag('js', new Date());

gtag('config', 'G-G640VE0Y19');

CME Group, the world's leading derivatives marketplace, today announced it will launch options on Eris SOFR Swap futures on June 15, 2026, pending regulatory review.

In the current landscape of shifting interest rate cycles and tightening liquidity, institutional hedgers are facing a silent drain on their balance sheets: initial margin (IM). While the transition from LIBOR to SOFR is behind us, participants continue to seek efficiencies in their hedging strategies within SOFR instruments.

Quarterly ADV for Q1 2026 climbed to 22,360 contracts ($2.2B notional), up 33% from Q4 2025. Eris SOFR also set a monthly volume record in March with 44,863 ADV, up 30% from the previous record from December 2025