Eris SOFR Swap Futures

Contract Specifications

For individual contract dates, fixed rate and key price/analytic variables, go to the Eris Contract Lookup Tool

| Exchange Listing | CBOT |

|---|---|

| Trading Hours | Globex trading hours (5:00pm CT to 4:00pm CT, Sunday to Friday) |

| Contract Notional | $100,000 for all tenors |

| Contract Structure | Contracts embed the exchange of receiving fixed annual amounts versus paying annual floating amounts. The floating amounts are determined from the daily compounded SOFR fixings during each Accrual Period |

| Trading Conventions | Long Futures Position Holder: Fixed Rate Receiver, Floating Rate (SOFR) Payer Short Futures Position Holder: Fixed Rate Payer, Floating Rate (SOFR) Receiver |

| Fixed Leg | Fixed rate, set to match the SIFMA SOFR MAC rate (set to the nearest 0.25% of the forward rate) |

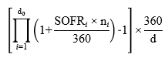

| Floating Leg | USD-SOFR-COMPOUND: rate set at the end of each Accrual Period, determined as the daily compounded value of SOFR fixings during the Accrual Period, where SOFRi is the daily SOFR fixings in the period, ni is the number of days covered by the SOFR fixing, and d is the number of days in the period

|

| Payment Frequency / Payment Dates | Annual for both Fixed and Floating Payments, paid 2 business days following the end of each Accrual Period, on an Actual/360 day count basis |

| Contract Listings | Quarterly IMM Effective Date Contracts (3rd Wednesday of March, June, September, and December of each year) |

| First Trade Date (Listing Date) | New contracts are listed for trading at the discretion of CME Group, typically approximately six months prior to the Contract Effective Date |

| Accrual Periods | Annual periods commencing on the Effective Date, to each subsequent annual calendar date thereafter, aligned with the Cash Flow Alignment Date (CFAD) and subject to adjustment in accordance with the Modified Following Business Day Convention. The end date of an Accrual Period is the start date of the next Accrual Period |

| Cash Flow Alignment Date (CFAD) | Date used for aligning fixed and floating Accrual Period end dates and determining the contract Maturity Date The Cash Flow Alignment Date (CFAD) is determined by adding the tenor in years to the Effective Date, and may fall on any calendar day, including weekends and holidays. For example, an Eris SOFR Future with an Effective Date of 12/16/2020 and a tenor of 3 years implies a Cash Flow Alignment Date of 12/16/2023, the calendar date 3 years following the Effective Date. Although 12/16/2023 is a Saturday, this date is still used to align annual Accrual Period End Dates. As 12/16/2023 is a Saturday, the final Accrual Period End Date rolls to Monday 12/18/2023, in accordance with the Modified Following Business Day Convention |

| Last Trade Date (Termination of Trading) | Trading terminates 2 business day before the Maturity Date, defined as 2 business days after final Accrual Period, which is the Effective Date + contract tenor years, aligned with Cash Flow Alignment Date (CAFD) and subject to Modified Following Business Day Convention (i.e., if that is not a USGS business day, then 1st business day after that. If next valid business day is in following month, the preceding valid USGS business day will be the Maturity Date) |

| Maturity Date | The date of final payment, which is two business days following the final Accrual Period end date. The Maturity Date may also be referred to as Termination Date |

| Remaining Tenor | The duration of time from today to the Cash Flow Alignment Date |

| Business Days | U.S. Government Securities market business days (SIFMA) |

| Tenors | 1Y | 2Y | 3Y | 4Y | 5Y | 7Y | 10Y | 12Y | 15Y | 20Y | 30Y |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Contract Code | YIA | YIT | YIC | YID | YIW | YIB | YIY | YII | YIL | YIO | YIE |

| Date Suffix | 3-characters: 1 character IMM Effective Month - Mar(H), Jun(M), Sep(U), Dec(Z), followed by a 2-digit effective year (e.g. YIWZ20 = Dec'20 Eris SOFR 5Y, maturing Dec'25) |

|---|---|

| Contract Price | Contracts cash settle for life to the Eris Price, capturing all the cash flows of the swap Eris Price = 100 + A(t) + B(t) - C(t)

|

| Price Increments | 100.0000 indexed decimal price to 4 decimal places, with minimum price increments equivalent to approximately 0.0015-0.0025% in yield. 1 full point (1.000) will represent $1,000.00 |

| Tenor Contract | 1Y YIA | 2Y YIT | 3Y YIC | 4Y YID | 5Y YIW | 7Y YIB | 10Y YIY | 12Y YII | 15Y YIL | 20Y YIO | 30Y YIE |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Initial Tick Size $/Px | $2.50 0.0025 | $2.50 0.0025 | $5.00 0.0050 | $10.00 0.0100 | $10.00 0.0100 | $10.00 0.000 | $20.00 0.0200 | $20.00 0.0200 | $20.00 0.0200 | $40.00 0.0400 | $40.00 0.0400 |

| Calendar Spread Tick Size $/Px | $2.50 0.0025 | $2.50 0.0025 | $2.50 0.0025 | $5.00 0.0050 | $5.00 0.0050 | $10.00 0.0100 | $10.00 0.0100 | $10.00 0.0100 | $10.00 0.0100 | $20.00 0.0200 | $20.00 0.0200 |

| Market Data Channel | 344 |

|---|

Eris Swap Futures Inter-Commodity Spreads

| ILink: Tag 55 Symbol MDP 3.0 Tag 1151 Security Group | EH |

|---|---|

| Tag 762 Security Subtype | IV-Intercommodity Spread |

| Product | Spread Name | Price Ratio* | Leg Quantity Ratio* | Minimum Price Increment |

|---|---|---|---|---|

| 1Y Eris SOFR Swap Future vs 2Y Eris SOFR Swap Future | EAT | 1.000 | 1:1 | .0025 or $2.50 |

| 1Y Eris SOFR Swap Future vs 3Y Eris SOFR Swap Future | EIC | 1.000 | 1:1 | .005 or $5.00 |

| 2Y Eris SOFR Swap Future vs 3Y Eris SOFR Swap Future | ETC | 1.000 | 1:1 | .005 or $5.00 |

| 2Y Eris SOFR Swap Future vs 5Y Eris SOFR Swap Future | ETW | 2.500 | 5:2 | .01 or $10.00 |

| 3Y Eris SOFR Swap Future vs 4Y Eris SOFR Swap Future | EID | 1.000 | 1:1 | .01 or $10.00 |

| 3Y Eris SOFR Swap Future vs 5Y Eris SOFR Swap Future | ECW | 1.666 | 5:3 | .01 or $10.00 |

| 4Y Eris SOFR Swap Future vs 5Y Eris SOFR Swap Future | EDW | 1.000 | 1:1 | .01 or $10.00 |

| 5Y Eris SOFR Swap Future vs 10Y Eris SOFR Swap Future | EIY | 2.000 | 2:1 | .01 or $10.00 |

| 5Y Eris SOFR Swap Future vs 7Y Eris SOFR Swap Future | EIB | 1.500 | 3:2 | .01 or $10.00 |

| 7Y Eris SOFR Swap Future vs 10Y Eris SOFR Swap Future | EBY | 1.500 | 3:2 | .02 or $20.00 |

* Leg quantity and price ratios are as of November 2023 and subject to change

Eris/Treasury Swap Spreads

PRODUCT | MDP 3.0: TAG 6937-ASSET | ILINK: TAG 55-SYMBOL | Price Ratio | Leg Quantity | Minimum Price Increment | GLOBEX INSTRUMENT CODE (NEAR TREASURY) | GLOBEX INSTRUMENT CODE (DEFERRED TREASURY) |

|---|---|---|---|---|---|---|---|

2-Year Eris SOFR Swap Futures (YIT) vs. 2-Year T-Note Futures (ZT) | ETU | ER | 1.000 | 2:1 | 0.0025 or $2.50 | ETU 02-01 Z23-Z3 | ETU 02-01 Z23-H4 |

5-Year Eris SOFR Swap Futures (YIW) vs. 5-Year T-Note Futures (ZF) | EWV | ER | 1.000 | 1:1 | 0.005 or $5.00 | EWV 01-01 Z23-Z3 | EWV 01-01 Z23-H4 |

7-Year Eris SOFR Swap Futures (YIB) vs. 10-Year T-Note Futures (ZN) | EBN | ER | 1.000 | 1:1 | 0.01 or $10.00 | EBN 01-01 Z23-Z3 | EBN 01-01 Z23-H4 |

10-Year Eris SOFR Swap Futures (YIY) vs. Ultra 10-Year T-Note Futures (TN) | EYT | ER | 1.000 | 1:1 | 0.01 or $10.00 | EYT 01-01 Z23-Z3 | EYT 01-01 Z23-H4 |

For more information about Eris SOFR vs Treasury Intercommodity Spreads on CME Globex, please visit CME Group's Website.